Article

10 min

Taking shelter from inflation

The clean energy transition remains a key theme in the infrastructure space, driven by a need to transform the energy sector from fossil fuel based to net zero by at least 2050. We believe there are two main ways to participate in this growth thematic across the global listed infrastructure universe: by owning renewables generation and by owning electric transmission and distribution networks. In some cases, investors can gain exposure to both these themes by investing in a single company, such as in the case of many US electric utilities.

One unique aspect about US electric utilities is that many are vertically integrated, meaning they are allowed to own both power generation assets as well as transmission and distribution assets. These investments all sit within the regulatory construct, allowing them to earn attractive, stable, regulated returns.

This differs from regulated electric utilities in Australia, the United Kingdom and Europe, which are generally only allowed to own transmission and distribution assets. To the extent utilities in these jurisdictions own renewables generation, they tend to sit outside the regulatory construct and earn returns based on contracted or merchant power prices.

We believe this nuance presents an exciting opportunity for investors, particularly because the US is still in the very early stages of the energy transition. With a significant proportion of US electricity still generated from fossil fuels, the opportunity to decarbonise existing generation fleets provides US vertically integrated utilities with multiple avenues to grow, both through investments in renewables generation and in the networks themselves.

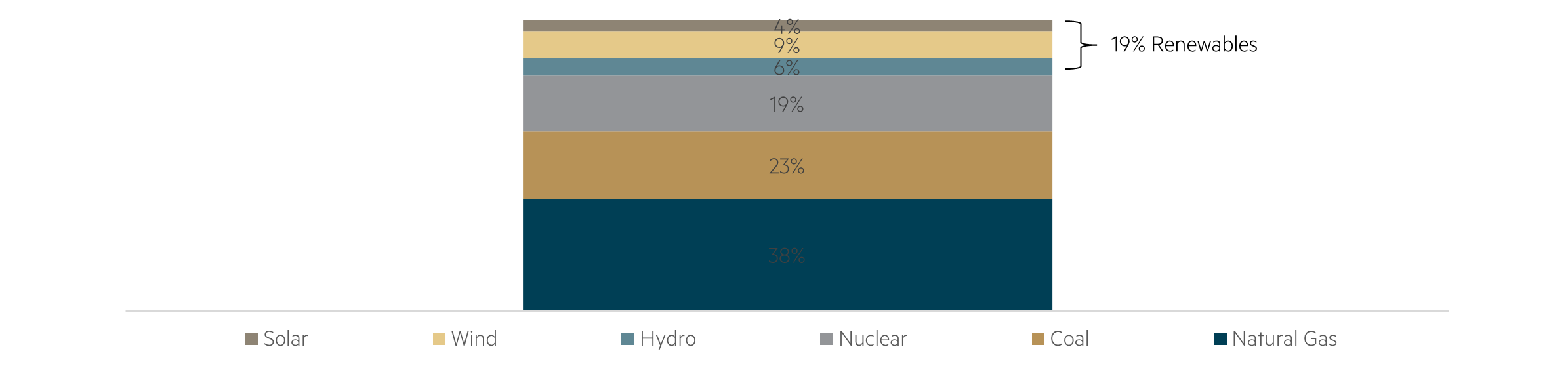

US electricity generation by source (2021)

Source: US EIA, Annual Energy Outlook 2022

AEP is one of the largest regulated electric utilities in the US and is also one of our largest positions. The company serves 5.5 million customers across 11 states and owns an extensive range of regulated generation, transmission and distribution assets. A significant proportion of AEP’s utilities are vertically integrated, although the company also operates in certain regions where they only own transmission and/or distribution. We believe AEP is a good example of a company that has multiple ways of winning in the clean energy transition.

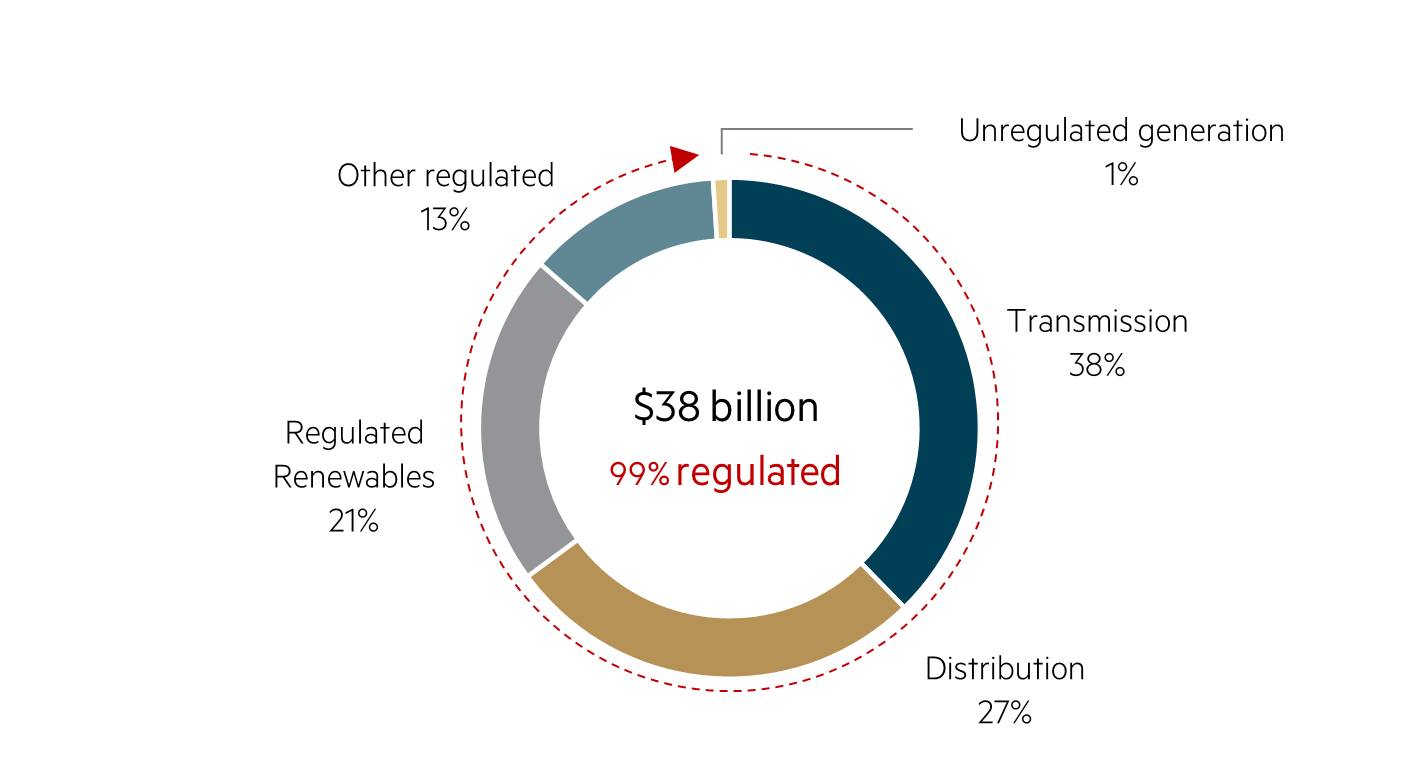

At the end of 2021, the company had a rate base of $56 billion and a $38 billion five-year investment plan, expected to drive rate base growth of 8% per annum between 2022 and 2026. Almost all of this will be regulated investments earning an allowed return of equity of above 9%, which will help drive the company’s targeted earnings per share growth of 6-7% per annum over the period.(1)

AEP's 5-year capital forecast (2022–2026)

Source: American Electric Power company filings

AEP’s story is particularly attractive because of its large exposure to transmission assets. Transmission networks are known to be the backbone of the grid, transporting electricity over long distances at high voltages from the source of generation to where customers need to use it. We believe there has been an increasing awareness towards the importance of transmission in facilitating the clean energy transition and addressing renewable bottlenecks. AEP owns the largest transmission system in the country, with a network that is over 40,000 miles long and includes more 765-kV extra-high voltage transmission lines than all other US transmission systems combined.

Recent transactions involving transmission assets also demonstrate how valuable these assets are to private owners. In 2021, Brookfield purchased a 19.9% minority interest in FirstEnergy Transmission for $2.4 billion, representing 40x P/E (trailing 12 months). In 2020, NextEra purchased a 100% stake in transmission operator GridLiance for $660 million, representing 1.9x rate base. These are much higher multiples than what AEP trades for today, which is approximately 20x P/E and 1.5x rate base.(2)

In addition to poles and wires, AEP also operate several vertically integrated utilities, which together own 23GW of regulated generation capacity, 12GW being coal. The company has committed to achieving net zero emissions by 2050, with an interim target of reducing emissions by 80% by 2030 and has established a timeline to decommission all remaining coal-fired power plants to support these goals. In tandem with this, the company expects it will need to invest in 15.2GW of replacement renewables capacity through 2030, of which only 5.8GW, or $8.2 billion, is included in their current capex plans.

In conclusion, we view AEP as a company at the heart of the clean energy transition. Not only is the company well positioned to benefit from the growth in transmission investment needed to facilitate more renewables, it also has a significant opportunity to invest in regulated renewable assets themselves through its vertically integrated utilities. Together, we believe this should provide a long runway of growth opportunities for the company extending beyond the current five-year plan.

How the energy transition is shaping infrastructure needs in the US (whitepaper)

1 Forward-looking estimates reflect company guidance as of Q4 2022

2 AEP’s multiples are based on MBA GLI estimates as of 31 March 2022

Disclaimer

This material was prepared and issued by Maple-Brown Abbott Ltd ABN 73 001 208 564, Australian Financial Service Licence No. 237296 (MBA). MBA is registered as an investment advisor with the United State Securities and Exchange Commission under the Investment Advisers Act of 1940. This information is intended solely for professional and institutional investors and is provided for information purposes only. This material is not intended for, and is not suitable for, retail clients and does not constitute investment advice or an investment recommendation of any kind and should not be relied upon as such. This information is general information only and it does not have regard to any investor’s investment objectives, financial situation or needs. Before making any investment decision, you should seek independent investment, legal, tax, accounting or other professional advice as appropriate. This material does not constitute an offer or solicitation by anyone in any jurisdiction. This material is not an advertisement and is not directed at any person in any jurisdiction where the publication or availability of the information is prohibited or restricted by law. Past performance is not a reliable indicator of future performance. Any comments about investments are not a recommendation to buy, sell or hold. Any views expressed on individual stocks or other investments, or any forecasts or estimates, are point in time views and may be based on certain assumptions and qualifications not set out in part or in full in this information. The views and opinions contained herein are those of the authors as at the date of publication and are subject to change due to market and other conditions. Such views and opinions may not necessarily represent those expressed or reflected in other MBA communications, strategies or funds. Information derived from sources is believed to be accurate, however such information has not been independently verified and may be subject to assumptions and qualifications compiled by the relevant source and this material does not purport to provide a complete description of all or any such assumptions and qualifications. To the extent permitted by law, neither MBA, nor any of its related parties, directors or employees, make any representation or warranty as to the accuracy, completeness, reasonableness or reliability of the information contained herein, or accept liability or responsibility for any losses, whether direct, indirect or consequential, relating to, or arising from, the use or reliance on any part of this material. This information is current as at 31 March 2022 and is subject to change at any time without notice.

© 2022 Maple-Brown Abbott

We use a tight definition of infrastructure assets with low-volatility cashflows and inflation protection to achieve diversification benefits with other asset classes, such as global equities.