Webcast

23 min

Whitepaper: How the energy transition is shaping infrastructure needs in the US

The Maple-Brown Abbott Global Listed Infrastructure (GLI) team invests in long-dated infrastructure assets that provide essential services – such as electricity, water, and transport – to people all around the world. As momentum builds to achieve net zero emissions by 2050, we see significant long-term opportunities for investors as the energy sector undergoes a once-in-a-lifetime transformation to decarbonise. In response, we have meaningfully shifted the GLI portfolio over the last two years to take advantage of the shift to a low carbon world.

Most recently, we published a research paper titled ‘The impacts of the energy transition on infrastructure needs in the US’, outlining a roadmap of opportunities to be realised through the energy transition; namely in renewables generation, transmission & distribution (T&D), electrification, and low carbon solutions. It is important to remind ourselves of the scale of investment needed to achieve net zero emissions by 2050. International energy bodies – the IEA and IRENA – state that $200 billion worth of annual investments will be needed in the North American power sector over the next 20–30 years, with IRENA modelling some 89% ($178 billion) for renewables and power grids alone.[i]

While impetus has been building for a number of years, the clean energy push has only intensified over the past 12 months despite the devastating effects of a global pandemic and a polarized political landscape in the US. From a global perspective, nine of the 10 largest economies (if we assume President Biden will fulfill his campaign promise) have now pledged to reach net zero emissions by 2050 to limit global warming in line with the goals of the Paris Agreement.

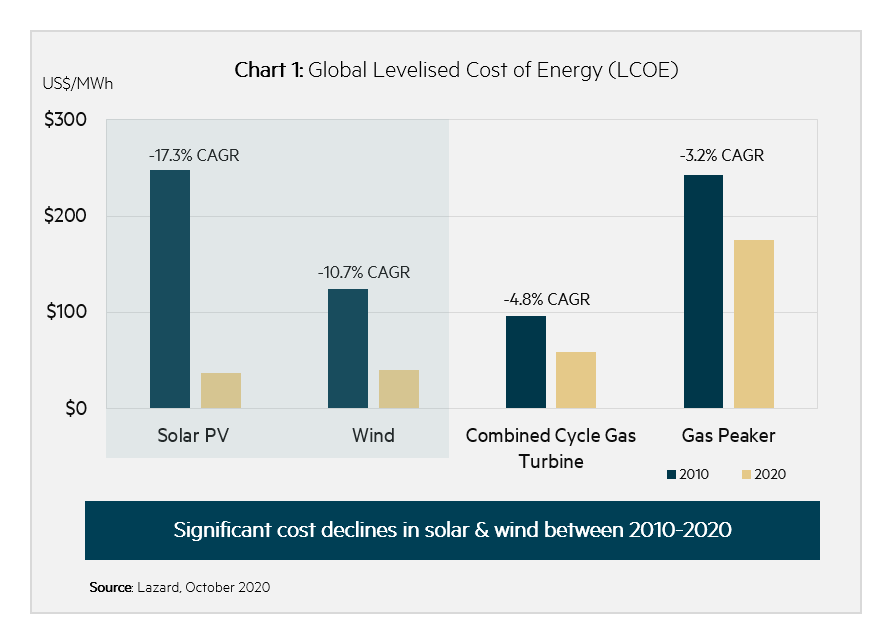

The energy transition is giving rise to opportunities for regulated electric utilities to grow their asset base and offer highly accretive earnings coupled with attractive allowed returns in a low interest rate environment. From our perspective, the improving economics of renewables over the last decade has, and continues to, stimulate strong growth for the sector. Indeed, between 2010 and 2020, the levelized cost of energy (LCOE) for utility-scale solar photovoltaic (PV) has fallen by 85% to $37/MWh while wind costs have declined by 70% to $40/MWh (see Chart 1).[ii]

Aside from the rapidly declining costs of renewables; improved scalability, federal tax incentives, and state-level policies are collectively facilitating the growth of renewables and the shift away from traditional generation, such as coal-fired power. Renewables adoption has ramped up from 11% to 18% of total US electricity generation between 2010 and 2020,[iii] with IRENA modelling uptake to reach 85% by 2050 under its Paris Agreement-aligned scenario.[iv] As recently discussed with the GLI team’s ESG Analyst, Georgia Hall, we are only at the beginning of a multi-decade journey towards renewable penetration.

We are frequently asked (and quite rightly) how customer bills can be kept affordable with these investments. With regulatory approval, utilities can increase equity earnings by shifting capital from generation plants requiring very large fuel inputs – such as coal-fired power plants – toward ones that run on free fuel, such as solar and wind. Commonly referred in the industry as “steel for fuel”, substituting “steel” in the form of new wind and solar generation facilities, for “fuel" used in power plants, can provide substantial operating cost savings to the utility and bill savings to customers. Reducing the fuel portion of consumers’ bills can also help insulate them from fuel cost volatility and potential liabilities.

Furthermore, renewables have lower operating & management (O&M) costs as they are less labour-intensive compared to traditional fossil fuel electricity generation. This all translates into an increase in regulated electric utilities’ asset base (on which it earns a return) alongside a decrease in O&M costs when replacing traditional fossil fuel plants with renewables. The combination of these factors, alongside others, will help keep electricity bills affordable for customers.

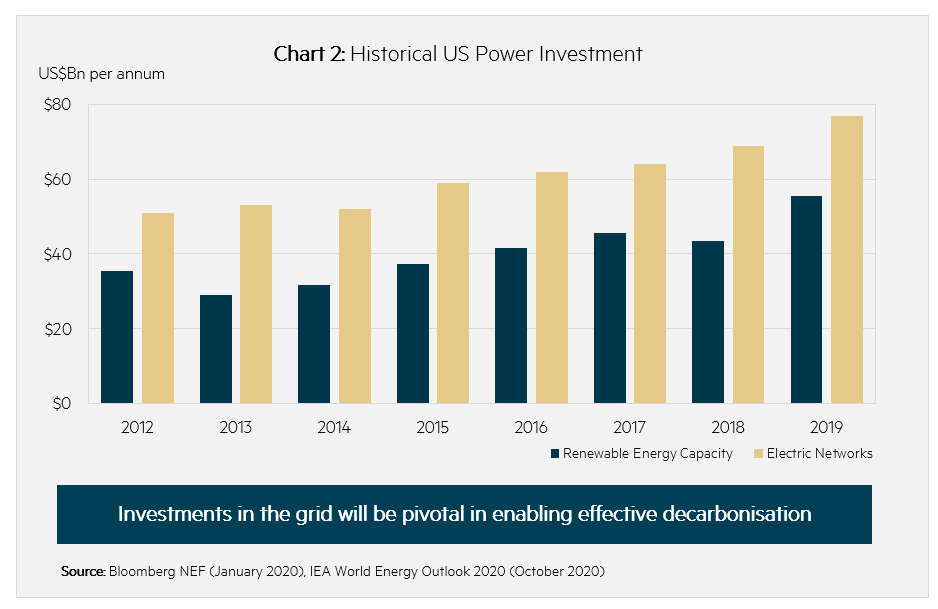

US electric utilities stand to not only benefit from significant investments in renewables generation – but also T&D infrastructure to help connect new sources of load and deal with a more complex grid. From our perspective, this is perhaps one of the most overlooked and underappreciated investment opportunities of the energy transition. Investments in the grid will be pivotal in enabling effective decarbonisation by ensuring reliability (by enabling interregional flows) and catering for the shift in the United States’ generation portfolio toward renewables and distributed energy resources.

“T&D infrastructure represents an enormous, multi-decade investment opportunity for the sector. These investments will be made almost entirely by the regulated utilities, which in turn will increase the regulated asset base, and therefore regulated returns, for investors.”

Grid investments in the US have stepped up materially over the past decade, growing by 11.6% year-on-year to reach $77 billion by 2019 (see Chart 2). The IEA forecasts that 3.3 million kilometres of electricity network lines will need to be built or replaced in the US through to 2030, with the majority being distribution lines, to meet existing energy and climate-related policy commitments.[v] T&D infrastructure represents an enormous, multi-decade investment opportunity for the sector. These investments will be made almost entirely by the regulated utilities, which in turn will increase the regulated asset base, and therefore regulated returns, for investors.

As ESG Analyst, Georgia explains, in reaction to these shifting dynamics, regulated US utilities companies are rapidly developing strategies centred around long-term decarbonisation goals with many targeting net zero emissions by 2050.

As part of our environmental, social, and governance (ESG) engagement program, we regularly meet with portfolio companies to dig into the details of their decarbonisation plans. As a fiduciary acting on behalf of our clients, we believe it is important for companies to produce a long-term strategy informed by climate scenario stress testing, stakeholder engagement, and robust right risk management and governance oversight to mitigate any potential stranded asset risk. On the GLI team, we have a long-standing commitment to integrating ESG into our investment process.

Our latest research paper covers off a host of other complex and interrelated variables, technologies, and dynamics on the horizon for the decarbonising energy sector. Topics span the future of natural gas networks, green hydrogen and renewable natural gas, battery storage, electric vehicles, and other emerging low carbon solutions.

Looking into the future, the key challenge faced by regulated utilities will be managing the energy transition whilst balancing competing factors of reliability, security, and affordability, and sustainability. As global energy needs continue to evolve, we believe it is critical for infrastructure investors to continue monitoring these trends, as they will have a significant impact on the growth outlook for these businesses.

Interested in investing with us?

We use a tight definition of infrastructure assets with low-volatility cashflows and inflation protection to achieve diversification benefits with other asset classes, such as global equities.