Article

4 min

Positive signs for global listed infrastructure in 2024

The imperative to mitigate climate change and reduce greenhouse gas emissions has propelled the world towards an energy transition, where reliance on fossil fuels is gradually being replaced by renewable energy sources and cleaner technologies. In the United States (US), utilities wield significant influence over the energy landscape, playing a central role in the generation, transmission and distribution of electricity. As such, US utilities are pivotal actors in driving the transition towards a more sustainable and resilient energy system.

For us, the attraction of US utilities is they earn a relatively high regulated rate of return and they are growing rapidly with the rollout of renewable energy technologies – which are supported by favourable tax credits. Electric utilities in particular remain attractive in our view and our internal valuations show several good opportunities.

We have built positions in key US utility assets in the Maple-Brown Abbott Global Listed Infrastructure Fund (the ‘Fund’) at what we believe are attractive prices, with the Fund having a 36% allocation to US utilities at the end of March.

Over the course of March our Global Listed Infrastructure investment team met with management teams from ten US utilities with a combined market capitalisation of over US$300bn. These meetings helped reinforce our positive views and opportunities on these critical enablers of the energy transition.

Technological innovations represent a cornerstone of energy transition, enabling US utilities to embrace cleaner and more sustainable energy sources. Renewable energy technologies, including solar photovoltaics (PV), wind turbines and energy storage systems, have undergone remarkable advancements in efficiency and cost-effectiveness. Solar and wind energy, once considered supplementary sources, are now competitive alternatives to conventional fossil fuels, bolstered by falling costs and performance improvements.

Moreover, the integration of digitalization and smart grid technologies has revolutionized grid management and operation for US utilities. Smart meters, sensors and advanced analytics provide utilities with real-time insights into energy consumption patterns, enabling them to optimise grid performance, enhance reliability and integrate renewable energy sources seamlessly. These technological advancements not only improve operational efficiency but also facilitate the transition towards more decentralised and resilient energy infrastructure.

The booming growth of data centers has been a consistent thematic in our discussion with US utility management teams, as these companies navigate the complexities of the energy landscape. Data centers serve as the backbone of our increasingly digital world, supporting everything from social media platforms to e-commerce giants and cloud computing services. Data centers are voracious consumers of energy, requiring vast amounts of electricity to power and cool their servers. This surge in energy demand presents utilities with an opportunity to expand their customer base and revenue streams. In addition to an expanded customer base, it is also about spreading the energy transition costs across more MWhs.

We expect several trends in the data center market for the next decade, including sustained market growth, hyperscaler growth, AI-driven disruption and a focus on power and sustainability. The availability of transmission capacity will become a key factor in data center interconnection. Access to economical and reliable power and water are critical factors for AI data center location. The long lead time of transmission planning versus the shorter timeframe to plan and build data centers creates a potential shortfall of transmission capacity, while pandemic-related shortages and insufficient domestic manufacturing capacity in the US all lead to potential delays in transmission project development.

The US is expected to be a key driver of data center growth and a March 2024 McKinsey and Company report suggested data center power demands will increase substantially in the US from 2023 to 2030 – adding ~250 TWh of new electricity demand, at a CAGR of ~15%. Power demand in the US has hardly grown from 2007 in aggregate, and data center load may make up 20-30% of all net new demand added between any two consecutive years until 2030.

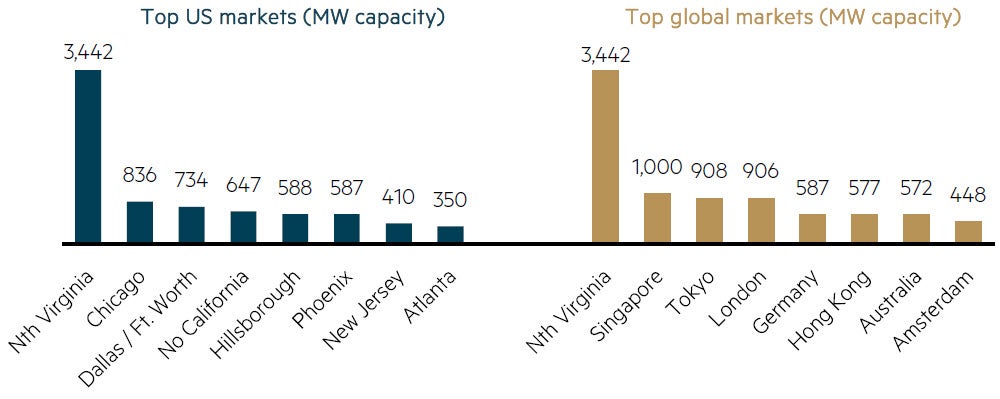

In our meetings, Dominion Energy (D), whose service territory includes Northern Virginia, stated Northern Virginia data center market is larger than the next five US markets combined and larger than the next four world markets combined*. Northern Virginia alone has 3,442 MW capacity as opposed to Tokyo at 908 MW and Australia with 572 MW.

Northern Virginia data center market is larger than the next five US markets combined and larger than the next four world markets combined

Source: Dominion Energy, Business Review Investor Meeting, PowerPoint Presentation (q4cdn.com) page 47. https://s2.q4cdn.com/510812146/files/doc_downloads/2024/2024-03-01-business-review-investor-slides-vTC.pdf. The chart used is solely for illustrative purposes. We do not claim any ownership or association with Dominion Energy. The use of this chart does not imply endorsement, sponsorship, or affiliation with Maple-Brown Abbott.

In a recent company update, Exelon Corporation (EXC) indicated they are seeing significant data center demand in the Chicago service territory for its subsidiary ComEd, with 5.6GW of new data center demand expected to come on line over the next few years**. The company has seen 400 MW of new demand from data centers since 2019.

In Ohio, American Electric Power (AEP) reported that data center demand currently makes up 12% of the company’s total commercial load. This figure is expected to increase to approximately one third of the commercial load by 2028***. In the third quarter of 2023, AEP experienced a 7.5% year-on-year commercial load growth, primarily driven by data center customers. The company anticipates several large projects to come online in 2025. From 2023 to 2026, AEP projects commercial load growth rates of 7.3%, 5.0%, 7.6%, and 4.1%, respectively^.

By providing reliable, resilient, and cost-effective power solutions tailored to the needs of data centers operators, utilities can capitalise on this growing market segment. The proliferation of data centers necessitates upgrades and enhancements to the existing grid infrastructure. By modernising the grid, utilities can improve reliability, enhance grid flexibility and accommodate the influx of intermittent renewable energy sources required to power data centers sustainably. Tech giants like Amazon, Google, Meta, Microsoft and Apple have all made a commitment to using 100% clean energy to power their data centers and utilities will be charged with partnering on those targets.

Electric vehicle (EV) adoption in the United States is experiencing rapid growth, driven by a combination of technological advancements, environmental concerns and supportive government policies. As EVs become increasingly mainstream, US utilities are poised to play a pivotal role in facilitating their widespread adoption and integration into the electric grid.

The widespread adoption of EVs presents both challenges and opportunities for grid management. Utilities must manage the increased electricity demand from charging vehicles while ensuring grid stability and reliability. US utilities are investing in the deployment of EV charging infrastructure to support the growing number of electric vehicles on the road. This includes the installation of public charging stations in urban areas, along highways and in commercial spaces. In California, new state policy requires 35% of new passenger vehicle sales in California must consist of zero-emissions vehicles by 2026, with the requirement increasing to 68% by 2030, and 100% in 2035. In 2023 a quarter of new cars sold in California were zero emission vehicles.

Still in California, despite the flat/declining population growth, utilities forecast strong load growth due to the electrification trend and growth in EVs. For Edison International (EIX) electric vehicles in Southern California Edison’s (SCE) service area added ~2,800 GWh of load in 2023 and could grow to 50,000+ GWh by 2045.

Effective regulatory frameworks are essential enablers that shape the trajectory of the energy transition for US utilities. Policies and regulations play a critical role in incentivising investment in renewable energy deployment, grid modernisation and energy efficiency initiatives. The Inflation Reduction Act (IRA) is climate legislation, passed by the United States congress in August 2022, that contains ~US$369bn worth of programs and funding to accelerate the transition to net zero carbon emissions in the US. The IRA’s rebates and credits will accelerate the electrification of energy utilization in homes and businesses, as well as boost the adoption of personal and commercial electric vehicles. Government policies and regulatory frameworks play a crucial role in shaping the EV market and providing incentives for adoption. Utilities advocate for supportive policies such as tax incentives, rebates and grants to accelerate EV adoption and infrastructure development. US Utilities are entering a transformational decade fuelled in part by the IRA.

Stakeholder engagement is paramount to the success of the energy transition for US utilities. Collaboration with policymakers, regulators, industry stakeholders and local communities fosters alignment of interests, facilitates knowledge sharing and promotes consensus-building. Engaging with customers and communities is essential to building trust, raising awareness and garnering support for clean energy initiatives.

Our Global Listed Infrastructure team remains actively engaged with all key stakeholders and engagement is an important pillar of our strategy to mitigate ESG risks and enhance value across the Fund’s holdings. In 2023, we joined the collaborative Climate Action 100+ (CA100+) engagement working group for American Electric Power. As one of our most emission intensive holdings, we believe collaborative engagement through the CA100+ initiative will be a powerful tool to complement our direct engagement efforts. You can read more in our Engagement & Stewardship Report.

US utilities are actively engaging with customers to raise awareness about the benefits of EVs and promote adoption. Outreach campaigns, incentives and education programs help dispel myths about EVs, address range anxiety and encourage consumers to make the switch to electric transportation.

Critical to the adoption of electrified technologies is the consumer. EIX has suggested that by 2045, electricity demand is projected to rise by over 80% from today, primarily due to electrification. Households are expected to benefit from savings well before 2045, with the average SCE household expected to see more than 10% savings by the early 2030s. These savings are expected to be driven by reduced fossil fuel expenses more than offsetting increase in electricity expenses, while improvements in equipment efficiency, energy efficiency and demand response programs reduce consumption.

The energy transition represents a transformative journey towards a more sustainable, resilient, and equitable energy future. US utilities play a pivotal role in this transition, empowered by key enablers such as technological innovations, regulatory frameworks, market dynamics, financial incentives and stakeholder engagement. By embracing cleaner energy sources, modernizing grid infrastructure and fostering collaboration with stakeholders, utilities can drive the transition towards a low-carbon future, while ensuring reliability, affordability and sustainability in the provision of energy services. As our recent interactions with key US utilities showed, collaboration between utilities, policymakers, regulators and stakeholders is essential to overcoming barriers and unlocking the full potential of the energy transition in the US.

* Dominion Energy, Business Review Investor Meeting, PowerPoint Presentation (q4cdn.com) page 47 The chart used is solely for illustrative purposes. We do not claim any ownership or association with Dominion Energy. The use of this chart does not imply endorsement, sponsorship, or affiliation with Maple-Brown Abbott.

** Exelon, Earnings Conference Call, Fourth Quarter 2023, https://investors.exeloncorp.com/static-files/08e9eefd-ab49-4675-b549-ad59756d5275, page 10

*** American Electric Power , AEP Load Addition Methodology, https://www.pjm.com/-/media/planning/res-adeq/load-forecast/aep-documentation.ashx, page 2

^American Electric Power, 58th Annual Edison Electric Institute Financial Conference, https://www.aep.com/Assets/docs/investors/eventspresentationsandwebcasts/2023EEI_Handout.pdf, page 19

Disclaimer

This information is prepared and issued by Maple-Brown Abbott Ltd ABN 73 001 208 564, AFSL. 237296 (‘MBA’) as the Responsible Entity of the Maple-Brown Abbott Global Listed Infrastructure Fund (‘Fund’). This presentation contains general information only, and does not take into account your investment objectives, financial situation or specific needs.

Before making a decision whether to acquire, or to continue to hold an investment in the Fund, investors should obtain independent financial advice and consider the current PDS and Target Market Determination (TMD) or any other relevant disclosure document of those products. For the Fund, the PDS, AIB and TMD are available at maple-brownabbott.com/document-library or by calling 1300 097 995.

Any views expressed on individual stocks or other investments, or any forecasts or estimates, are not a recommendation to buy, sell or hold, they are point in time views and may be based on certain assumptions and qualifications not set out in part or in full in this document. Information derived from sources is believed to be accurate, however such information has not been independently verified and may be subject to assumptions and qualifications not described in this document. To the extent permitted by law, neither MBA, nor any of its related parties, directors or employees, make any representation or warranty as to the accuracy, completeness, reasonableness or reliability of this information, or accept liability or responsibility for any losses, whether direct, indirect or consequential, relating to, or arising from, the use or reliance on this information. Units in the Fund mentioned in this presentation are issued by MBA.

The chart used is solely for illustrative purposes. We do not claim any ownership or association with Dominion Energy. The use of this chart does not imply endorsement, sponsorship, or affiliation with Maple-Brown Abbott.

This information is current as of 15 April 2024 and is subject to change at any time without notice.

© 2024 Maple-Brown Abbott Limited.

Interested in investing with us?

We use a tight definition of infrastructure assets with low-volatility cashflows and inflation protection to achieve diversification benefits with other asset classes, such as global equities.