Article

2 min

Value stock or value trap?

We have been of the view for some time that inflation would likely prove to be ’sticky’ and thus interest rates would remain higher for longer. Given the sharp rise in interest rates, the resilience of the Australian consumer has surprised most commentators. To date, consumers appear to have generally coped well as fixed rate loans continue to reprice (much) higher, although it is still early days. More recently we have seen a softening in consumer discretionary spending, although thus far it has been ’less bad than feared’. This view was supported by solid trading updates from several discretionary retailers during the August reporting season:

Buoyed by results such as these, the Consumer Discretionary sector was the best performing sector in the August reporting season.

In a similar vein, the credit data reported by Australian banks during August showed what we perceive to be very benign trends. While stressed exposures have increased modestly, this is off a very low base. As such, credit losses remain below long term averages. We favour the banks – also beneficiaries of higher rates – with our positive view premised on two attributes: inexpensive valuations and sensible earnings forecasts.

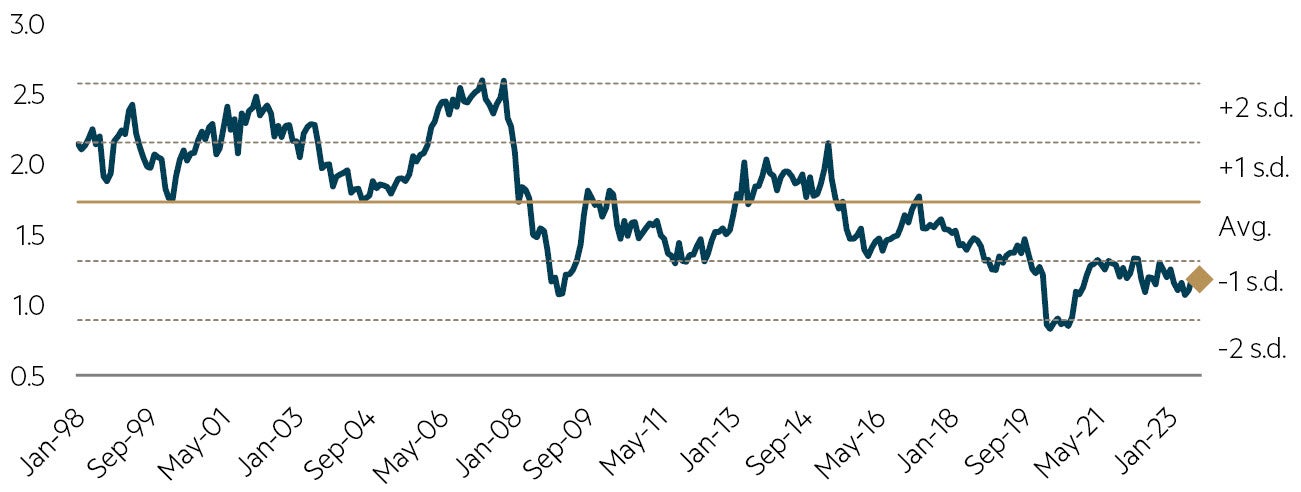

The chart below highlights the price to book valuation metric of the banks, excluding Commonwealth Bank (the one bank which remains overpriced in our view). Collectively, the other banks are trading in line with where they bottomed out in the GFC and only modestly above where they bottomed out in the pandemic. While return on equity will be lower for the banks today than in prior years, largely due to increased capital requirements (and thus improved resilience), it appears to us that bank share prices are already discounting tough conditions.

Source: IRESS, Goldman Sachs Global investment research, data to 30 September 2023. Past performance is not a reliable indicator of future performance.

The second attraction of the banks is that earnings forecasts appear ’sensible’, particularly when compared to some of the ‘high flying’ industrial stocks (which we will look at later). Of course, almost all forecasts will be ’wrong’ but for the banks, the market expects low single digit credit growth, ongoing Net Interest Margin (or NIM) compression, modest expense growth and increasing credit charges. Our forecasts are similar. This produces a relatively flat earnings profile; however, we forecast most banks can still generate a satisfactory total return to investors, largely driven by high single digit gross dividend yields (including franking). Further upside exists if our credit charges prove too pessimistic, which has been the case so far, and the potential for modest capital management.

Within the equity market, one of the few beneficiaries of rising interest rates are the general insurers: they collect premiums upfront, invest the so-called ’free float’ before ultimately paying out claims. As the free float is generally invested in cash and short-dated fixed interest, returns improve as interest rates rise. While the general insurers are also impacted by climate change, via increased claims and re-insurance costs, the recent Bureau of Meteorology announcement of the arrival of an El Nino climate pattern should help reduce the incidence of costly natural disasters this summer in Australia. We remain favorably disposed to the general insurers.

We have been writing for some time about the extended multiples many stocks within the Industrials sector continue to trade on. During the pandemic Industrials (ex-Financials) peaked at ~30 times forward earnings. As this was an average, many stocks traded far higher. For example, CSL, at the time the largest stock in our equity market, traded on ~45 times forward earnings! Since then, as interest rates have risen, Industrials sector multiples have fallen somewhat, but still (on average) are around one standard deviation more expensive compared to history at ~22 times.

In addition to expensive multiples, many of the favoured industrial stocks were also trading on elevated earnings and / or elevated earnings expectations. Over the course of the most recent reporting season, and indeed the ’confession’ season that now precedes it under the continuous disclosure regime, some of these stocks started to unravel. In most cases it was the inability of the company to deliver the lofty earnings expectations that the market demanded to essentially justify the share price.

Fallen Angels

But multiples still elevated

| Stock* | Market Cap1 A$ billion | Earnings Downgrade2 | Peak-to-Trough3 Price Fall | Consensus P/E4 (x) |

| CSL | 121 | -9% | -19% | 26 |

| ResMed | 35 | -1% | -40% | 21 |

| WiseTech Global | 21 | -19% | -26% | 74 |

| REA Group | 20 | -2% | -7% | 42 |

| Reece | 12 | -7% | -10% | 33 |

| ASX | 11 | -7% | -22% | 23 |

| S&P/ASX 300 Index | -6% | -6% | 15 |

*Past performance is not a reliable indicator of future performance

1 FactSet as at 30 September 2023.

2 Revision in FactSet FY24e consensus EPS over the 6-month period ending 30 September 2023.

3 Within the 6-month period ending 30 September 2023.

4 FactSet consensus 12-month forward P/E as at 30 September 2023.

The table above highlights the plight of some of these ‘fallen angels’. As an example, CSL provided a trading update in June that led to consensus FY24 earnings being downgraded ~10% resulting in a share price that has subsequently fallen almost twice that. In fairness to CSL, it isn’t that earnings are expected to go backwards, CSL is still forecast to grow earnings in FY24 by around 12% in USD. However, for investors it was enough that CSL missed the market’s ambitious earnings forecasts for the stock to be punished.

We continue to monitor these so-called fallen angels but haven’t invested in any yet as even after the downgrades and a derating many still screen as expensive. While we are unlikely to be investing in WiseTech Global on ~75 times earnings (better than the 100 times it peaked at!), there are other names that are starting to look interesting. We do believe that after a decade (or longer) of falling interest rates, it will take some time for the higher rate environment to be priced appropriately by equity markets. As such, we believe patience may be required but will ultimately be rewarded. In the meantime, our portfolios are tilted towards the beneficiaries of higher rates such as the banks and general insurers.

Market commentators continue to focus on the macroeconomic environment both here and overseas, and a chorus of bears continue to recite their recessionary lines. As bottom-up stock pickers we are alert to the broader environment but remain focused on in-depth analysis at the stock level and structuring our portfolios to take advantage of emerging pockets of longer-term value.

Disclaimer

This information was prepared and issued by Maple-Brown Abbott Ltd ABN 73 001 208 564, Australian Financial Service Licence No. 237296 (‘MBA’). This information must not be reproduced or transmitted in any form without the prior written consent of MBA. This information does not constitute investment advice or an investment recommendation of any kind and should not be relied upon as such. This information is general information only and it does not have regard to any person’s investment objectives, financial situation or needs. Before making any investment decision, you should seek independent investment, legal, tax, accounting or other professional advice as appropriate, and obtain the relevant Product Disclosure Statement and Target Market Determination for any financial product you are considering. This information does not constitute an offer or solicitation by anyone in any jurisdiction. This information is not an advertisement and is not directed at any person in any jurisdiction where the publication or availability of the information is prohibited or restricted by law. Past performance is not a reliable indicator of future performance. Any comments about investments are not a recommendation to buy, sell or hold. Any views expressed on individual stocks or other investments, or any forecasts or estimates, are point in time views and may be based on certain assumptions and qualifications not set out in part or in full in this information. The views and opinions contained herein are those of the authors as at the date of publication and are subject to change due to market and other conditions. Such views and opinions may not necessarily represent those expressed or reflected in other MBA communications, strategies or funds. Information derived from sources is believed to be accurate, however such information has not been independently verified and may be subject to assumptions and qualifications compiled by the relevant source and this information does not purport to provide a complete description of all or any such assumptions and qualifications. To the extent permitted by law, neither MBA, nor any of its related parties, directors or employees, make any representation or warranty as to the accuracy, completeness, reasonableness or reliability of the information contained herein, or accept liability or responsibility for any losses, whether direct, indirect or consequential, relating to, or arising from, the use or reliance on any part of this information. Neither MBA, nor any of its related parties, directors or employees, make any representation or give any guarantee as to the return of capital, performance, any specific rate of return, or the taxation consequences of, any investment. This information is current at 31 October 2023 and is subject to change at any time without notice. You can access MBA’s Financial Services Guide here for further information about any financial services or products which MBA may provide. ©2023 Maple-Brown Abbott Limited.

Interested in investing with us?

We are a disciplined Australian equities value manager that has been managing Australian equities since we were established in 1984. Over time we have made refinements to our investment process, however our commitment to value investing remains unchanged.